Decision Tree Analysis

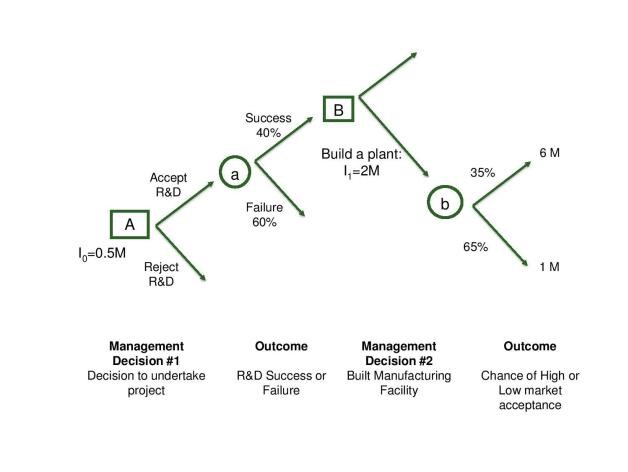

Decision Tree Analysis (DTA) is one of the tools that is used to account for uncertainty and encapsulates the later decisions by the management. It is useful for analyzing sequential investment decisions at discrete points of time. In DTA, the management is faced with a sequence of decisions that they have to choose based on the alternatives that provide maximum NPV of the project. To illustrate, let us assume company A decides to invest in R&D. The initial investment would be around half a million Euros. Based on the past information or valuable future information, the management believes that there could be 40% chances of success of R&D. If the R&D is successful, they have to invest further to build a plant that has a 35% chance that the market will be highly receptive of the product and a 65% chance that it would be medium chances of acceptance. The decision tree would look like this:

Figure: Decision Tree denoting outcome at each node. Square node: management decision, Circle node: outcome There are two different types of nodes here. Square nodes denote the decisions of management whereas the circle nodes denote the outcomes i.e. decisions not completely under the control of management. The management decides whether or not to accept R&D at node A. If it does, the nature will make a move at the node a to reveal the outcome. It is important to note that the management’s initial decision affects the future events and decisions. Assuming that the later decisions are optimal, the decisions at present will be obtained by folding back the tree from the end. The purpose of this article is not to deal with the numbers but to understand the feasibility of DTA. Despite the fact that it is well suited for analyzing sequential investment decisions, it has following limitations:

- Cost of capital(discount rate): The figure denotes a very simplistic scenario. In real life, there could be many branches at various nodes and calculating discount rates each year at different decision points is very complex and it would be incorrect to use the same discount rate in each phase.

- The DTA could become unmanageable in real life scenarios when the branches expand geometrically

- In real life, the decision choices such as Option to Delayor Option to Expand may not occur at discrete points rather they could occur continuously and might require management’s constant supervision.

So what’s the solution? Real options As discussed in my last VIEW post, real options can eliminate these challenges. We will discuss more about Real options in the next VIEWS post.

– Saurabh Mishra

Leave a Comments