The Value of Intangibles

Do Intangible assets have different set of rules to value them? The answer is No. It’s only because of accounting rules that allow them to look differently. The accounting rules are consistent in their treatment of manufacturing companies but it does not do a good job in case of Intangible assets. The pharmaceutical/biotech companies whose main intangible assets are R&D are expensed instead of capitalized[1]. Let us analyze the ramifications of treating R&D as an operating expense than capitalizing it:

- Cash flowsfrom existing Intangible assets: The capital expenditures that are associated with R&D are mis-categorized as operating expenses; hence the earnings that we see in the Income statement is not a true measure of earnings

- Growth rate:A Company can grow only when it reinvests and earn excess returns. If we expense the R&D costs which is so critical for the growth of pharmaceutical companies, we are unable to calculate how much the company is reinvesting and how well it is reinvesting

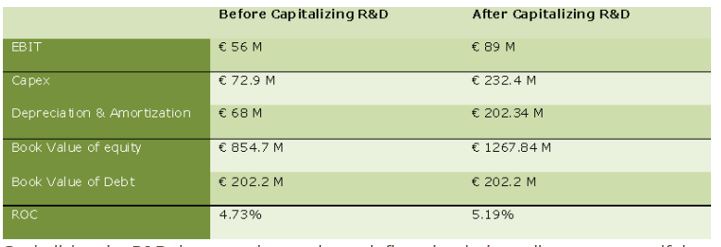

In order to see the difference on R&D adjustments as Capex, let’s see the example of Almirall that we valued in March 2013

Capitalizing the R&D does not change the cash flows but it does allow one to see if the R&D is adding value or not. In this case, the return on capital after capitalizing has increased slightly. This shows the R&D productivity of Almirall. Those companies who have very high productivity of R&D will have very high return on capital on capitalizing that will increase the value of the company ( assuming they earn excess returns) and those who have poor R&D productivity will have return on capital less than that without capitalizing. [1] Under IFRS a certain portion of development costs are capitalized where as in US GAAP R&D costs are treated as operating expenses